In many companies, differences in supplementary pension arrangements persist based on employee status. For example, a group insurance plan may apply to white-collar staff members only, or different contribution levels may exist for blue-collar workers. The Law on Complementary Pensions requires these differences to be harmonised by 2030. What does this mean in practice? What's required, what's allowed and what's often misunderstood?

Why harmonisation?

For a long time, the distinction between "predominantly manual work" and "predominantly intellectual work" led to different employment conditions, and a great deal of dissatisfaction. In reality, the differences between blue- and white-collar status are not always logical, particularly when employees perform similar roles or when the line between manual and intellectual work becomes blurred. In the interest of fairness, transparency and legal certainty, the Law of 26 December 2013 introduced the single employment status for blue- and white-collar workers, covering notice periods, the first sick day and related measures.

For supplementary pensions, the social partners agreed on a gradual harmonisation between blue- and white-collar workers. This agreement was enshrined in the Law on Complementary Pensions1. One important clarification: the single employment status applies to supplementary pension entitlements, death benefits and waiver of premiums coverage included in the second pension pillar. It does not apply to incapacity benefits or medical expenses.

For you as an employer, this legal framework offers clear guidance to review your group insurance plans step by step and align them with future requirements. A good understanding of the rules is essential to avoid misunderstandings and unnecessary risks.

1 Article 14 of the LCP, amended by the Law of 5 May 2014 (RD of 9 May 2014) and the Law of 12 December 2021 (RD of 31 December 2021)

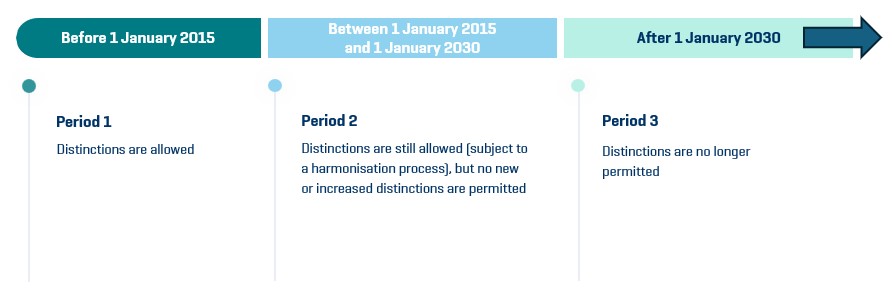

The legal framework: 3 key periods

Lawmakers opted for a phased approach, with clear milestones for sectors and companies. The objective is clear: by 2030, all differences in supplementary pensions based solely on blue- or white-collar status must be eliminated.

Three employment periods are relevant:

Note: Harmonisation does not mean that every employee must have the exact same pension plan. Differentiation remains possible, as long as it is based on objective and reasonable criteria, such as job classification or role level. This point is often misunderstood - unfortunately so, as these misunderstandings can lead to poor decisions or procrastination.

3 common misconceptions about second pillar harmonisation

"We can compensate pension differences with salary or bonuses."

That isn't possible. Equality must be achieved within the pension plan itself, not through other forms of pay or benefits.

"Everyone must have exactly the same pension plan."

Not necessarily. Differences are allowed, provided they are objectively justified and not based solely on blue- or white-collar status.

"We can wait until just before the deadline to take action."

Adopting a wait-and-see attitude is risky. Employers must be able to demonstrate that they are actively working towards harmonisation, supported by analyses, simulations and proposals discussed in social dialogue.

Why early action pays off

Differences in pension accrual cannot be compensated through other benefits. Alignment has to happen within the pension system itself. Because pension plan harmonisation is often part of broader collective bargaining negotiations, the legislation deliberately provides a long transition period. Used effectively, that time allows employers to move forward step by step:

- Know your starting point

Do you still have different pension plans for blue- and white-collar workers? Identify existing differences early on. - Track sector-level developments

Sectors play a decisive role during this transition phase. Their CBAs may shape your available options. - Think ahead towards 2030

Harmonisation takes time. The legislation expects employers to start preparing well in advance. This preparation may include analyses, simulations and consultation, enabling informed decisions. Exploring scenarios early helps avoid time pressure and unexpected costs.

Your AG contact person will be happy to review your group insurance with you and identify the appropriate next steps towards a legally sound, attractive and future-proof pension policy. Feel free to schedule an appointment.