Return to Work

Help your employees who are unable to work due to illness to return to work sustainably and up to three times faster.

More info

Employees in Belgium are taking extended sick leave in skyrocketing numbers, and the figures keep rising every year. While our social security system provides a financial safety net, state benefits are quite modest, enough to cover essential living expenses only.

You'll be providing your staff members with more than a financial cushion. You can enhance the well-being of your staff members with My Mind by AG, and get them back to work safely, successully and sustainably with a custom-designed return-to-work assistance programme in the event of a stress-related mental disorder.

A more competitive salary package

An accident, critical illness, stress, burnout, maternity leave... there are multiple reasons to be off work for an extended period.

With Income Care, your staff members will have a monthly replacement income to fall back on if ever they are off on occupational incapacity leave.

In the first month of occupational incapacity leave, staff members will still collect 100% of their salary, payable by the employer.

Between the 2nd and the 12th month, the employer generally stops paying their staff for sick leave. Instead of a paycheck, they’ll have to rely on state benefits, which are just 60% of their gross salary.

After one full year, the occupational incapacity will be reclassified as a disability. Staff members will then be entitled to an allowance according to their marital/family status, which is for example just 40% of the gross salary if married or in a registered domestic partnership.

When calculating the disability benefit, the INAMI/RIZIV applies a maximum annual salary cap of EUR 58.281,60 or EUR 4.856,80 on a monthly basis (last update: March 2026). The higher the salary, the greater the loss of income.

Anything above this cap, but also other earnings and benefits such as year-end bonuses, performance bonuses, meal vouchers, etc., are excluded from the calculation.

Employees aren't always aware of this salary cap. 2 out of 3 employees overestimate the size of the state benefits they'd be entitled to collect.

Want to check the size of your state benefits yourself? Try our simulation tool.

In addition to being a must-have for your staff members, income protection insurance also offers several interesting benefits for you as an employer:

Barely 1 out of 5 employees in Belgium have occupational incapacity coverage. By offering a group income protection plan, you can differentiate your company and raise your profile as a caring employer, an important attribute for many job seekers in the current market.

Research shows that employees greatly value income protection insurance. This type of coverage gives you a competitive edge in the war for talent.

With Income Care, you’ll help move your company to the top of your candidates’ consideration list and have an extra sweetener to retain your top talent.

What's more, according to our study published in the "Cost of Absenteeisme" whitepaper, the positive emotional environment created by a caring climate can significantly impact how staff members feel and function in their professional lives. In short, working for a caring employer reduces the risk of stress-related absences.

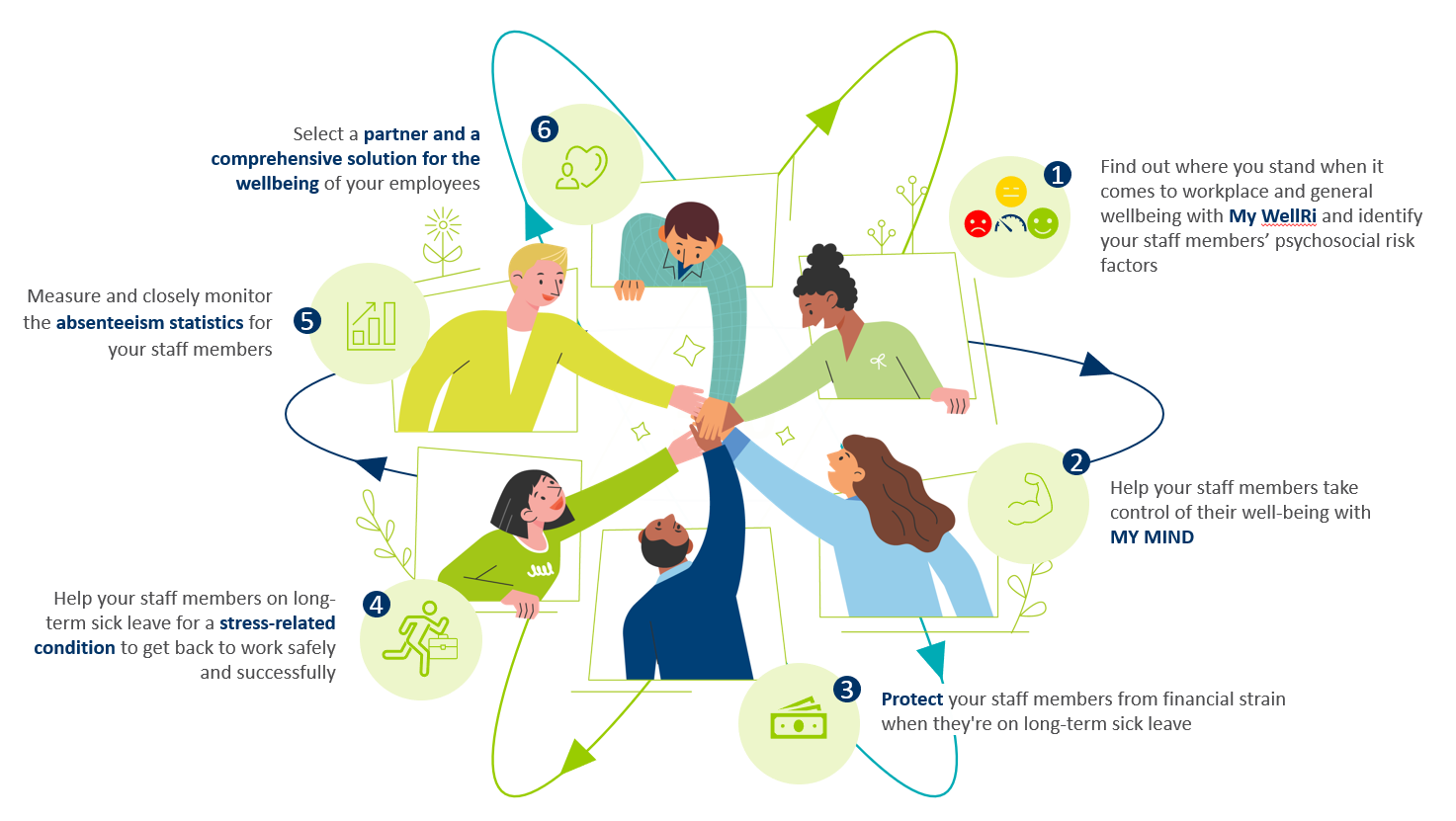

Offering a financial safety net is no longer enough: a holistic approach is what's needed to prevent long-term absenteeism.

As the first market player to include Return to Work assistance in its insurance coverage as of 2017, AG has continued to meet the needs of its customers by also launching prevention services in 2019, now under the name of Waldon:

In addition, for certain customers (if they can preserve the anonymity of the data), a Return to Work dashboard is available to track the evolution of mental disorders, measure employee satisfaction with the solution, and compare their results with other companies.

Income Care offers a solution for many employees, but also for you. With this coverage, you can raise your profile as a caring employer. For optimum protection, you determine the scope of coverage yourself, depending on your company's needs.

Select the covers to be included

Set the insured risk

Select the incapacity benefit type

Customise the coverage and select

You'll find more details on how Income Care works in this handy guide.

And, of course, you are always welcome to contact us if you have any questions or need individually-tailored advice. Send in your questions about income protection insurance or request a non-binding quote for Income Care, and we’ll get back to you as soon as we can.